In 2019, U.S. fed cattle producers and beef buyers filed class action antitrust lawsuits against the four largest beef packers in the country: Tyson Foods, JBS USA, Cargill, and National Beef Packing Company. The plaintiffs alleged that these companies engaged in an unlawful conspiracy with the purpose of decreasing fed cattle prices and increasing wholesale and retail prices of beef as early as January 2015 and thus violated Section 1 of the Sherman Act (1890). This article examines competition (business conduct) issues in light of the alleged price-fixing cartel revealed during the on-going cattle and beef antitrust litigation.

The U.S. beef packing industry is highly concentrated, with approximately 85% of market share held by the four largest firms (beef packers) in fed cattle slaughtering (U.S. Department of Agriculture, Agricultural Marketing Service, 2022). While several economically significant acquisitions took place in the industry in the last two decades, these acquisitions did not alter the number of the largest beef packers. Some of these acquisitions affected the ownership of the largest beef packers.

In 2001, Tyson Foods (now the largest U.S. meat processor) acquired Iowa Beef Processors, then the largest U.S. beef packer (Ward, 2010). In 2007, JBS S.A. (a Brazilian company and the world’s largest meat processor) acquired Colorado-based Swift Foods Company (then the third largest U.S. beef processor). As of 2007, the four largest beef packers in the United States were Tyson Foods (market share of 23.6%), Cargill Meat Solutions (market share of 22.0%), JBS USA (market share of 14.6%), and National Beef Packing Company (market share of 11.4%); Smithfield Beef Group was the fifth-largest beef packer (marketshare of 6.5%) (Livestock Marketing and Competition Issues, 2009). In 2008, JBS S.A. acquired Smithfield Beef Group (Johnson, 2009). In 2018, Marfrig(a Brazilian company) purchased the controlling ownership interest in National Beef Packing Company (National Beef Newsroom, 2018).

The U.S beef packing industry also has a high degree of vertical coordination (Greene, 2019). While the spot (cash) market for fed cattle was the dominant marketing arrangement among fed cattle producers and beef packers in the industry prior to the 2000s, the use of alternative marketing arrangements—particularly the use of forward and formula contracts—has increased in the last 20 years. For example, the share of fed cattle sold in a traditional negotiated spot (cash) market setting decreased from approximately 55% in 2004 to 23% in 2019 (Greene, 2019, Figure 1). In contrast, the share of fed cattle sold using forward and formula contracts increased from approximately 31% in 2004 to 70% in 2019.

Both forward contracts and formula contracts establish a price determination method for the price to be determined later, when fed cattle are delivered to the beef packing plants. Forward contracts use the Chicago Mercantile Exchange live cattle futures contract prices as a base to determine the actual price paid to fed cattle producers. Formula contracts use spot (cash) market prices as a base to determine the actual price paid to fed cattle producers. The spot (cash) market prices used in formula contracts are typically those reported by the USDA Agricultural Marketing Service.

In their complaints filed in the court, fed cattle producers and beef buyers argued that a price-fixing conspiracy among the four largest beef packers affected fed cattle and beef price dynamics, beginning in 2015. The complaints state that the four largest beef packers implemented the following, allegedly anticompetitive and coordinated supply restraints to decrease the quantity offed cattle purchased and slaughtered and consequently the quantity of beef produced, which ultimately decreased fed cattle prices and increased wholesale and retail prices of beef (In Re: Cattle Antitrust Litigation: Ranchers Cattlemen Action Legal Fund United Stockgrowers of America et al. v Tyson Foods, Inc. et al., 2019; Pacific Agri-Products v. JBS USA Food Company Holdings et al., 2019; and Peterson et al. v. Agri Stats, Inc. et al., 2019).

• Periodically reduced fed cattle slaughter volumes to reduce the demand for fed cattle.

• Periodically decreased the purchase and slaughter of cash cattle (fed cattle purchased in the spot (cash) market).

• Coordinated their procurement (purchasing) practices for cash cattle.

A decrease in the quantity of cash cattle purchased and coordinated cash cattle procurement decreased the spot (cash) price for fed cattle, which consequently caused formula contract prices to decrease (formula contracts use spot prices as reference prices).

• Simultaneously closed and/or idled plants to further decrease the slaughter capacity, refrained from expanding the plant capacity, and operated some of their plants at a reduced processing capacity (reduced hours, scheduled maintenance shutdowns, etc.).

• Imported foreign cattle at a loss to reduce domestic demand.

The complaints discuss a significant change in price dynamics throughout the beef supply chain beginning in 2015, which affected the profitability of beef packers. For example, the beef buyers’ complaints mention that fed cattle prices steadily increased between 2009 and 2014, and wholesale prices of beef moved in tandem. As a result, profit margins of the beef packers were very small, in the range of 1% to 4%. The beef buyers argued that the beef packers implemented coordinated supply restraints to increase their profit.

In 2015, while fed cattle prices began to decrease, wholesale and retail prices of beef were increasing, causing profit margins to increase. Tyson and JBS (both are public companies) discussed in the Earning Calls with their investors increased profit margins, in the range of 4% to 8%, obtained due to their visibility into the beef supply chain and their ability to balance fed cattle supply and beef product demand. Tyson and JBS emphasized that their goal was to operate a “margin business”, rather than a “market share business”.

The plaintiffs claimed that the alleged input and output price-fixing cartel of the four largest beef packers violated Section 1 of the Sherman Act (1890). This Section prohibits contracts, combinations, and conspiracies in restraint of trade in interstate commerce. Price-fixing agreements (cartels or conspiracies) aim to increase, decrease, or fix (stabilize) product prices, and can be verbal, written, or inferred from the conduct of firms (Federal Trade Commission, 2022).

Fed cattle producers and buyers purchasing beef directly from the beef packers aim to recover treble damages under the Clayton Act (1914). Buyers purchasing beef indirectly from the beef packers (for example, final consumers) aim to recover damages in selected states, where consumer protection laws, antitrust laws, or unjust enrichment laws allowing indirect buyers to recover damages exist.

In their responses to the complaints, the four largest beef packers argued that agricultural supply and demand conditions, not a price-fixing conspiracy, affected fed cattle price dynamics (In Re Cattle Antitrust Litigation: Memorandum of Law in Support of Defendants’ Joint Motion to Dismiss the Consolidated Amended Class Action Complaint, 2019). The beef packers argued that the allegedly anticompetitive practices described in the complaints were elements of lawful independent competitive behavior:

• Periodic slaughter reductions took place in a period of declining fed cattle supply, which was—prior to 2015—the beginning of the alleged price-fixing conspiracy. Slaughter volumes increased beginning in 2015.

• Reduced purchases of cash cattle also took place in the period of declining fed cattle supply, which was prior to 2015. Given that approximately 70% of fed cattle are purchased using forward and formula contracts, it is economically rational to decrease purchases of fed cattle in the spot (cash) market in a period of declining fed cattle supply.

• The types of allegedly coordinated fed cattle procurement practices used in the spot (cash) market were consistent with lawful competition, based on past court analysis and economically rational behavior of beef packers.

• Three of the four alleged plant closures took place before the beginning of the alleged price-fixing conspiracy. These plant closures were not simultaneous.

• A slight increase in the import of fed cattle from Canada and Mexico was observed since 2015, because it was economically rational for the beef packing plants located near the borders with Canada and Mexico to import foreign cattle rather than domestic cattle from distant geographic areas.

At the beginning of 2022, JBS reached a $52.5 million settlement agreement with buyers who had purchased beef products (boxed or case-ready beef) directly from JBS (Beef Direct Purchaser Class Action, 2023). At the beginning of 2023, JBS reached a $25 million settlement agreement with commercial and institutional buyers who had purchased beef products (boxed or case-ready beef) indirectly from JBS (Beef Antitrust Litigation Settlement, 2023). In the settlement agreements, JBS denied any wrongdoing.

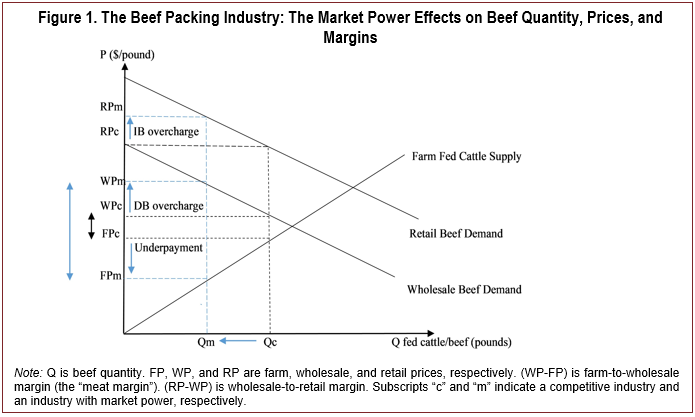

The U.S. Department of Justice (U.S. and Plaintiff States v. JBS S.A. and National Beef Packing Company, LLC., 2008) conveniently explains the economics of market power in the beef packing industry:

“With the price of fed cattle representing most of the cost of beef production, packer profitability is determined largely by the “meat margin,”[1] or the spread between the price packers pay for fed cattle and the price packers charge for beef, including USDA-graded boxed beef.

This meat margin is highly sensitive to changes in the aggregate output levels of fed cattle packers. All else being equal, when the meat packing industry reduces production levels, feedlots and cattle producers are paid less for fed cattle because fewer fed cattle are demanded and customers pay more for USDA-graded boxed beef because less is available for purchase.

Because the supply of fed cattle and the demand for USDA-graded boxed beef are relatively insensitive to short term changesin price, even small changes in industry production levels can significantly affect packer profits.” [emphasis added]

Figure 1 demonstrates price effects of market power in the beef packing industry consistent with this explanation. This figure also depicts underpayment to fed cattle producers and overcharges attributed to beef buyers that are the basis for damages that plaintiffs aim to recover during the ongoing cattle and beef antitrust litigation. The total underpayment to fed cattle producers (in U.S. dollars) is the “Underpayment” rectangle in this figure. The total overcharges attributed to direct buyers (DB) and indirect buyers (IB) (in U.S. dollars) are the “DB overcharge” and “IB overcharge” rectangles, respectively. Food retailers purchasing beef directly from beef packers are an example of direct buyers. Final consumers purchasing beef from food retailers are an example of indirect buyers.

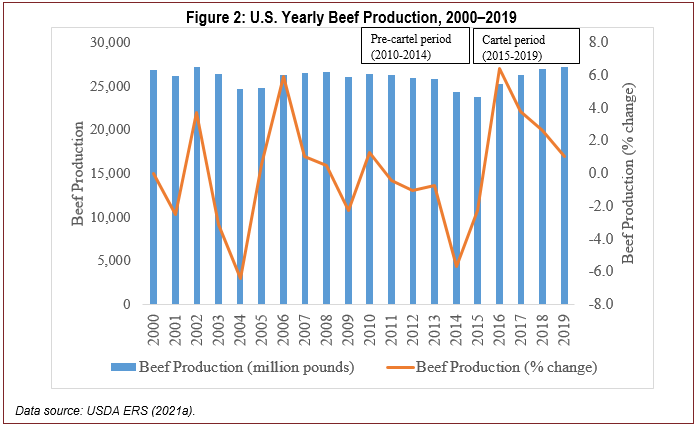

Following decreasing fed cattle inventory and increasing fed cattle prices (U.S. Government Accountability Office, 2018), yearly beef production was decreasing in the pre-cartel period (2010–2014). Increasing beef production in the cartel period (2015–2019) (see Figure 2) followed increasing fed cattle inventory and decreasing fed cattle prices.

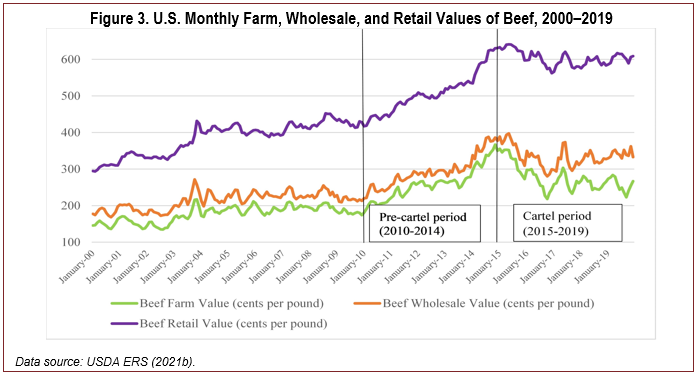

Compared with the pre-cartel period, monthly average farm, wholesale, and retail values of beef and the monthly average farm-to-wholesale and wholesale-to-retail margins increased, but the monthly average farm sector share decreased in the cartel period (Bolotova, 2022). The beef values are proxies for prices received by fed cattle producers, beef packers, and beef retailers (Hahn, 2004).

The monthly average farm value of beef increased from $2.60/lb per pound in the pre-cartel period to $2.74/lb in the cartel period, or by 5.4% (Figure 3). The monthly average wholesale value of beef increased from $2.94/lb in the pre-cartel period to $3.34/lb in the cartel period, or by 13.6%. The monthly average retail value of beef increased from $5.09/lb in the pre-cartel period to $6.03/lb in the cartel period, or by 18.3%.

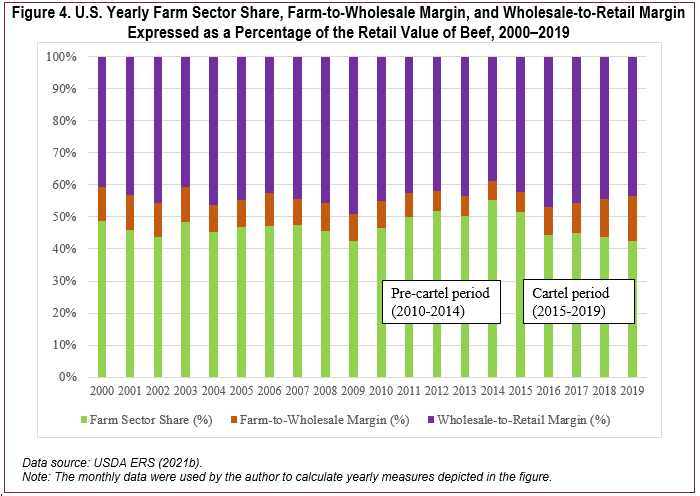

The monthly average farm sector share decreased from 50.77% of the retail value of beef in the pre-cartel period to 45.39% in the cartel period, or by 10.6% (Figure 4). The monthly average farm-to-wholesale margin (the “meat margin”) increased from 6.78% of the retail value of beef in the pre-cartel period to 10.02% in the cartel period, or by 47.6%. The monthly average wholesale-to-retail margin increased from 42.44% of the retail value of beef in the pre-cartel period to 44.59% in the cartel period, or by 5.1%. The observed increase in the farm-to-wholesale margin in the cartel period may be due to increases in beef processing costs and/or a short-run increase in profit due to market power of the beef packing industry.

The empirical evidence suggests that beef pricing by beef packers was consistent with perfectly competitive pricing in the pre-cartel period and with oligopoly and monopoly pricing in the cartel period (Bolotova, 2022). Beef pricing by food retailers was consistent with oligopoly pricing in both periods. Beef packers and food retailers shifted to a beef price stabilization practice in the cartel period, which might have contributed toincreases in the wholesale and retail values of beef as well as in the farm-to-wholesale and wholesale-to-retail margins in the cartel period. Earlier academic research evaluating market power in the U.S. beef packing industry prior to 2012 reports either no evidence of market power or a small market power magnitude (MacDonald et al., 2000; Crespi, Xia, and Jones, 2010; Ward 2010; Cai, Stiegert, and Koontz, 2011).

Competition concerns on a high level of concentration in the U.S. beef packing industry, the largest beef packers’ buyer and seller market power, and the increasing use of alternative marketing arrangements for fed cattle—which the largest beef packers can allegedly use to manipulate fed cattle prices—will likely remain in the future. The modern fed cattle market is characterized as thin because the share of fed cattle sold in the spot (cash) market is relatively small compared to the share sold using alternative marketing arrangements (Adjemian et

al., 2016). To some extent, thin markets lack market and price transparency, and they may be prone to market and price manipulations. In 1999, the Livestock Mandatory Reporting Act established a livestock mandatory price reporting program to improve the flow of market information and price discovery process in livestock markets, which was ultimately expected to enhance competition in the markets for livestock and livestock products (Greene, 2019). This act requires beef packers to report prices, quantities, and other transaction-specific information related to the purchases of fed cattle and sales of boxed beef daily to the USDA Agricultural Marketing Service responsible for enforcing the act. This information is processed and posted for public access on the USDA Agricultural Marketing Service webpage.

The availability of price and other market information for industry participants facilitates transparent price discovery and increases market efficiency, which generally has substantial procompetitive effects, with no harm to competition involved. However, in the case of imperfectly competitive industries, publicly available price and other market information may facilitate information exchanges among competitors, some of which may have anticompetitive effects (Bloom, 2014). The firms with market power can use price and other market information to facilitate their tacit or overt collusion and to effectively enforce it. Tacit collusion is a coordinated conduct of firms with market power that does not involve an explicit agreement among them in violation of Section 1 of the Sherman Act. Overt collusion is a coordinated conduct of firms with marketpower that involves an explicit agreement among them, which would violate Section 1 of the Sherman Act.

There are opinions expressed in academic literature that may suggest that the Livestock Mandatory Reporting Act might have created opportunities for tacit collusion in the beef packing industry (Wachenheim and DeVuyst, 2001; Cai, Stiegert, and Koontz 2011). In addition, some livestock producers expressed concerns that packers manipulated the USDA Agricultural Marketing Service Livestock Mandatory Reporting system (U.S. Department of Justice, 2012).

To inform future policy directions, systematic research is required to understand the potential for the largest beef packers to exercise market power and engage in collusive conduct. The first research direction would be to assess the current Livestock Mandatory Reporting system to determine whether any elements of this system create potential for beef packers to manipulate the system and/or facilitate tacit collusion among beef packers.

The second research direction would be to apply price variance screens for collusion to data available from the USDA Agricultural Marketing Service, including Livestock Mandatory Reporting data. Both tacit and overt collusion of firms operating in concentrated industries can affect price variance and higher moments of price distribution (Connor, 2006; Harrington, 2008). The screens for collusion—particularly price variance screens—have been discussed in academic literature and applied in a variety of industry settings (Bolotova, Connor, and Miller, 2008; Abrantes-Metz and Bajari, 2009). Research in these directions can assist in market monitoring efforts and inform future policy directions affecting the U.S. beef packing industry and the entire beef supply chain.

Abrantes-Metz, R.M., and P. Bajari. 2009. “Screens for Conspiracies and Their Multiple Applications.” Antitrust 24:66–71.

Adjemian, M.K., B.W. Brorsen, W. Hahn, T.L. Saitone, and R.J. Sexton. 2016. Thinning Markets in U.S. Agriculture What Are the Implications for Producers and Processors? U.S. Department of Agriculture, Economic Research Service. Economic Information Bulletin EIB-148.

Bloom, M. 2014. Information Exchange: Be Reasonable. Federal Trade Commission, Bureau of Competition. Available online: https://www.ftc.gov/news-events/blogs/competition-matters/2014/12/information-exchange-be-reasonable

Bolotova, Y.V. 2022. “Competition Issues in the U.S. Beef Industry.” Applied Economic Perspectives and Policy 44:1340–1358.

Bolotova, Y., J.M. Connor, and D.J. Miller. 2008. “The Impact of Collusion on Price Behavior: Empirical Results from Two Recent Cases.” International Journal of Industrial Organization 26:1290–1307.

Cai, X., K.W. Stiegert, and S.R. Koontz. 2011. “Oligopsony Fed Cattle Pricing: Did Mandatory Price Reporting Increase Meatpacker Market Power?” Applied Economic Perspectives and Policy 33:606–622.

Connor, J.M. 2006. “Collusion and Price Dispersion.” Applied Economics Letters 12:335-338.

Crespi, J.M., T. Xia, and R. Jones. 2010. “Market Power and the Cattle Cycle.” American Journal of Agricultural Economics 92:685–697.

Greene, J.L. 2019. Livestock Mandatory Reporting Act: Overview for Reauthorization in the 116th Congress. Congressional Research Service. Report R45777.

Hahn, W. 2004. Beef and Pork Values and Price Spreads Explained. U.S. Department of Agriculture, Economic Research Service. Report LDP-M-118-01.

Harrington, J.E. 2008. “Detecting Cartels.” In Paolo Bucirossi, ed. Handbook of Antitrust Economics. Cambridge, MA: MIT Press.

Johnson, R. 2009. Recent Acquisitions of U.S. Meat Companies. Congressional Research Service. Report RS22980.

Livestock Marketing and Competition Issues. 2009. Congressional Research Service. Report RL33325.

MacDonald, J.M., M.E. Ollinger, K.E. Nelson, and C.R. Handy. 2000. Consolidation in U.S. Meatpacking. U.S. Department of Agriculture, Economic Research Service, Food and Rural Economics Division. Agricultural Economic Report AER-785.

National Beef Newsroom. 2018. April 9. “Marfrig Purchases National Beef Ownership Interest.”

U.S. Department of Agriculture, Agricultural Marketing Service. 2022. Agricultural Competition: A Plan in Support of Fair and Competitive Markets. USDA’s Report to the White House Competition Council.

———. 2023. Livestock Mandatory Price Reporting. https://www.ams.usda.gov/rules-regulations/mmr/lmr

U.S. Department of Agriculture, Economic Research Service (USDA ERS). 2021a. Food Availability Data System: Red Meat. https://www.ers.usda.gov/data-products/food-availability-per-capita-data-system/

———. 2021b. Historical Price Spread Data for Beef, Pork, Broilers. https://www.ers.usda.gov/data-products/meat-price-spreads/

U.S. Department of Justice. 2012. Competition and Agriculture: Voices from the Workshops on Agriculture and Antitrust Enforcement in our 21st Century Economy and Thoughts on the Way Forward.

U.S. Government Accountability Office. 2018. U.S. Department of Agriculture Additional Data Analysis Could Enhance Monitoring of U.S. Cattle Market. Report GAO-18-296.

Wachenheim, C., and E. DeVuyst. 2001. “Strategic Response to Mandatory Reporting Legislation in the U.S. Livestock and Meat Industries: Are Collusive Opportunities Enhanced?” Agribusiness 17:177–195.

Ward, C. 2010. “Assessing Competition in the U.S. Beef Packing Industry.” Choices 25(2).

Beef Antitrust Litigation Settlement. 2023. https://www.beefcommercialcase.com/

Beef Direct Purchaser Class Action. 2023. https://beefdirectpurchasersettlement.com/

In Re Cattle Antitrust Litigation: https://www.docketbird.com/court-cases/In-Re-Cattle-Antitrust-Litigation/mnd-0:2019-cv-01222

In Re Cattle Antitrust Litigation: Memorandum Opinion and Order Granting Defendants’ Motions to Dismiss dated September 28, 2020.

In Re Cattle Antitrust Litigation: Memorandum of Law in Support of Defendants’ Joint Motion to Dismiss the Consolidated Amended Class Action Complaint dated September 13, 2019.

In Re Cattle Antitrust Litigation: Ranchers Cattlemen Action Legal Fund United Stockgrowers of America et al v Tyson Foods, Inc. et al 2019. Class action complaint filed by fed cattle producers on May 07, 2019.

Peterson et al v. Agri Stats, Inc. et al 2019. Class action complaint filed by indirect buyers on April 26, 2019. https://www.hbsslaw.com/uploads/case_downloads/beef-antitrust/2019-04-26-hagens-berman-beef-antirust-class-action-lawsuit-complaint.pdf

Pacific Agri-Products v. JBS USA Food Company Holdings et al 2019. Class action complaint filed by a direct buyer on October 16, 2019. https://www.courtlistener.com/recap/gov.uscourts.mnd.183132/gov.uscourts.mnd.183132.1.0.pdf

U.S. and Plaintiff States v. JBS S.A. and National Beef Packing Company, LLC. 2008. https://www.justice.gov/atr/case-document/complaint-137

Bolotova, Y.V. 2022.“Competition Issues in the U.S. Beef Industry.” Applied Economic Perspectives and Policy 44:1340 1358. https://onlinelibrary.wiley.com/doi/10.1002/aepp.13179

[1] Author’s note: The “meat margin” includes beef processing cost and profit of beef packers.